Landfill Tax

The Landfill Tax in the UK is applied to wastes that go to Landfill, which increases the overall cost of Landfill. The tax is applied per tonne of waste, applied in addition to the gate fee charged by the landfill operator, who is responsible for charging and collecting the tax from the disposer of the waste, and accounting for the tax and paying it to HMRC.

In 2024/25 tax year the amount of Landfill Tax collected was £486 million which was £3 million lower than the previous year[1]. VAT is charged on the combined Landfill gate fee and the Landfill Tax.

Historical Context

The Landfill Tax was introduced in 1996 and was the UK's first environmental tax.

The tax was seen as a key mechanism in enabling the UK to meet its targets set out in the Landfill Directive for the reduction in the landfilling of Biodegradable Municipal Waste.

Through increasing the overall cost of landfill, recycling and other waste treatment technologies with higher gate fees (which divert biodegradable waste from landfill) were made to become more financially attractive.

From 2015 the Scottish Landfill Tax[3] came into force (at the same rates England and set for the same rate in 2019/20) and from April 2018 Wales [4] set its own landfill tax known as the Landfill Disposal Tax (with a slightly higher rate for active waste 2019/20 of £91.70). Since 2020/21 Wales, Scotland, Northern Ireland and England have been been aligned. [5][6].

Arrangements

There are two rates of landfill tax, the lower rate which is applied to specfieid waste materials by HMRC (previoulsy referred to as the 'inactive rate' due to its linkage to wastes that are generally considered to have a lower rate of environmental pollution such as concrete, brick, glass, soil, clay and gravel ) and the standard rate which are all wastes not captured by the lower rate (previously referred to as the 'active rate' due to its linkage to wastes with a higher potential for environmental pollution such as wood, duct work, piping, plastics and mixed residual waste )[2].

For some wastes specific testing is necessary to demonstrate it is eligible for the lower rate. This is especially the case for Process Fines that fall into the category of Qualifying Material - essentially the testing required is a Loss of Ignition Test (LOI) to demonstrate that less that 10% of the material is organic in nature.

There have been an increasing number of exemptions agreed over time and operators have in the past mitigated their tax liability by the utilisation of these exemptions for certain sites (i.e. quarries that require restoration with inert soils) and for certain uses in a landfill sites (i.e. by using waste derived stone to replace virgin stone used in engineering/construction of a site)[2].

These exemptions, and the increasing divergence between landfill tax rates (with evidence of this being linked to increasing illegal activities) led to a consultation by HMRC to change the approach to Landfil Tax in April 2025, with responses published in November 2025[9]. Measures to ensure the gap does not increase will be introduced and issues with Qualifying Fines are likely to evolve in the future.

Comparison Between Landfill Tax and Recycling Rates

The Landfill Tax started out at modest rates and annual increases, and increased by £8 per tonne from 2006 to 2014 before moving closer to inflationary increases thereafter (see table at bottom of page)

Notes

- Increases in LFT have broadly driven recycling rates (and other waste treatment), especially with the steps from 2006 to 2014 - the graph shows the Waste from Households Recycling Rate for the UK up to 2023, the most recent year available[8]

- LFT has essentially 'flat-lined' since 2014 by following inflationary increases, and recycling levels have also flat-lined

- For context the 22% substantial increase for the 2025/26 tax year to £126.15 was roughly x4 the landfill gate fee[10]

Landfill Tax Credit Scheme

Landfill operators are able to make payments to organisations that qualify under the Landfill Communities Fund under the Landfill Tax Credit Scheme, rebating a proportion of the landfill tax collected for qualifying community or environmental projects in the vicinity of a landfill sites and is regulated by ENTRUST, with £37.8 million[1] rebated in the 2017/18 tax year. No figures were stated in the March 2026 release.

Historical Rates and Tax Collection

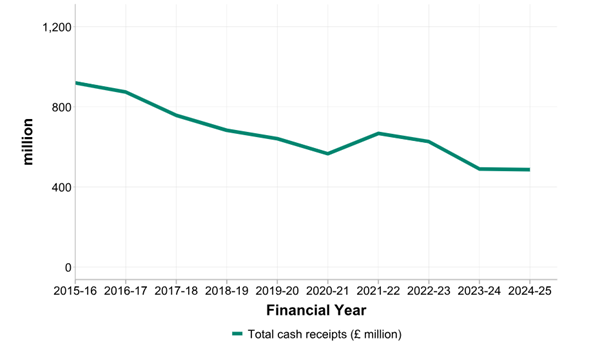

Total Landfill Tax Receipts

Notes

- The graph on the left is an extract from the Environmental Taxes Bulletin[1]

- The graph is figure 4 from the bulletin - total LFT receipts

- Rates have dropped over the last 10 years which reflects a drop in landfilling

- However, the proportion of waste at lower rates has increased in proportion to the total, partially reflecting the increased number of exemptions utilisied by companies and also speculation that waste is illegally being misclassified to avoid tax.

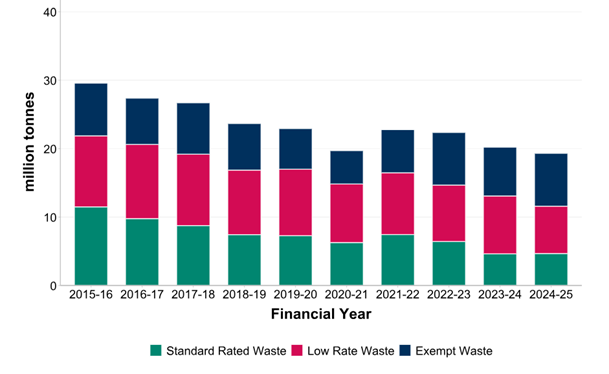

Landfill Tax Receipts by Tonnage

Notes

- The graph on the left is an extract from the Environmental Taxes Bulletin[1]

- The graph is figure 6 from the bulletin - LFT split by tonnage, taxable tonnage of which received and exempt by financial year

- Total tonnage has dropped over 10 years, standard rate has dropped consistently, with a small increase in the last year as a result of the stepped increase in tax rate

- Lower rate as a proportion of total tonnage has increased by 40%, and exempt by 40% in 2025 - this has supported many commentators speculating that waste is illegally being misclassified to avoid tax.

Historical and Current Landfill Tax Rates

Financial Year | Standard Rate | Lower Rate |

|---|---|---|

1996/97 | £7.00 | £2.00 |

1997/98 | £7.00 | £2.00 |

1998/99 | £7.00 | £2.00 |

1999/00 | £10.00 | £2.00 |

2000/01 | £11.00 | £2.00 |

2001/02 | £12.00 | £2.00 |

2002/03 | £13.00 | £2.00 |

2003/04 | £14.00 | £2.00 |

2004/05 | £15.00 | £2.00 |

2005/06 | £18.00 | £2.00 |

2006/07 | £21.00 | £2.00 |

2007/08 | £24.00 | £2.00 |

2008/09 | £32.00 | £2.50 |

2009/10 | £40.00 | £2.50 |

2010/11 | £48.00 | £2.50 |

2011/12 | £56.00 | £2.50 |

2012/13 | £64.00 | £2.50 |

2013/14 | £72.00 | £2.50 |

2014/15 | £80.00 | £2.50 |

2015/16 | £82.60 | £2.60 |

2016/17 | £84.40 | £2.65 |

2017/18 | £86.10 | £2.70 |

2018/19 | £88.95 | £2.80 |

2019/20 | £91.35 | £2.90 |

2020/21 | £94.15 | £3.00 |

2021/22 | £96.70 | £3.10 |

2022/23 | £98.60 | £3.15 |

2023/24 | £102.10 | £3.25 |

2024/25 | £103.70 | £3.30 |

2025/26 | £126.15 | £4.05 |

2026/27 | £130.75 | £8.65 |

References:

- HMRC National Statistical Environmental Bulletin commentary (March 2026)

- General Guide to Landfill Tax LFT1

- Scottish Landfill Tax

- Landfill Disposals Tax (Wales)

- Letsrecycle Article

- Excise Note LFT1 updated 9 April 2020

- Letsrecycle

- Graph by Monksleigh

- Consultation on Reform of Landfill Tax in England and Northern Ireland: Summary of Responses (HMRC Nov 2025)

- Landfill Tax:: increases in rates from 1st April 2026